(Image credit: Getty Images)

Editor’s note: This is the third article in a five-part series about all-asset retirement planning that is covering such topics as using annuities and housing wealth, making the most of tax benefits and managing investment portfolio risk. Articles one and two are It’s Time to Redefine Retirement for Retirees With $500,000 to $5 Million: Here’s How and Unlock Housing Wealth and Tax Benefits by Adding Lifetime Annuities to Your Retirement Plan.

For most Baby Boomers, their home represents 50% of their net worth, yet retirement planning software and advisers virtually ignore this asset in designing retirement income plans.

A Federal Reserve study shows that the share of net worth in primary residences among households headed by people ages 60 to 69 rose from roughly 40% in 1989 to just over 50% by 2022.

Sign up for Kiplinger’s Free Newsletters

Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Profit and prosper with the best of expert advice – straight to your e-mail.

For those age 70 to 79, the share climbed from about 38% to 50% over the same period. In the 15 million mass affluent households led by Boomers from age 60 to 75, the principal residence has an average home equity of $750,000, out of an average net worth of $1.75 million.

In this article, we explore the reasons housing wealth is ignored and why consideration of it can increase retirement income and liquid savings to cover large health-related and uncovered expenses.

Reasons housing wealth is not included in planning

Most retirement planning leaves out housing wealth and ignores the potential of that wealth to generate income or produce liquid savings. This is despite the fact that reverse mortgages, mostly home equity conversion mortgages (HECMs), are heavily marketed.

Our research indicates that planning tools often treat HECMs simply as a “liability for loans made” rather than as a “dynamic liquidity asset” that grows over time. In fact, most planning systems treat a HECM and its growing line of credit essentially as a swap for selling the house to access that cash.

Some reasons for this planning limitation:

Possible objections to HECM. Common arguments include high closing costs and service fees, along with the fear of having the home taken because the loan eats up its value. Also, the “common wisdom” has often been “no mortgages in retirement.”

Planning only for income. Income is essential, but full and robust retirement planning should also meet the objectives for liquidity and legacy. The Three L’s — Lifetime Income, Legacy and Liquidity — address retiree objectives and should drive planning strategies and tactics.

Just like a business plan, if you prepare and decide first on the objectives of the Three L’s, you will significantly improve your chances for a successful retirement.

Adviser licensing. Those advisers doing retirement planning for prospects or clients might be licensed to execute only a portion of a plan, from investments to lifetime annuities and finally to HECM.

They or their firms must form partnerships to implement a plan with all the product solutions that should be considered. That may require one or more large financial firms to create these partnerships or internal organizations that are multi-licensed.

Adviser training and available software. Advisers are often taught to think that housing wealth is a significant but relatively illiquid asset for retirees, which is true if selling the house or borrowing through a traditional home loan are the only approaches considered for accessing equity. Very few planning systems consider the HECM line of credit to provide liquidity.

I’ve read about these reverse mortgage objections from pundits and heard the same from friends, but as we are focused on providing the best retirement planning results, we had to do our own analysis.

Why housing wealth should be included in planning

Here are some reasons to include housing wealth in your retirement planning:

Addressing unmet needs. As I wrote in the previous article in this series, Unlock Housing Wealth and Tax Benefits by Adding Lifetime Annuities to Your Retirement Plan (link above), a HECM used with lifetime annuities can help mass affluent retirees secure additional lifetime income, tax advantages and liquid savings to cover late-in-life expenses beyond what their 401(k) or IRA savings alone could provide.

Events like long-term care or additional support for children and home renovation when aging in place are unpredictable, which is why an additional source of liquid savings, like a HECM, may be essential.

Cost of accessing liquid savings. There is significant savings in being able to access the value of the home without selling it. The average cost of selling a home is 10% to 15% of its sales price, not to mention the stress involved with moving.

In addition, if the house is sold at a gain, the tax cost can be another 10% to 20% — meaning that selling a house now worth $2 million to generate liquid savings might have a total cost of $250,000 or more.

Special HECM protection. HUD backs every HECM loan, ensuring that the borrower’s family will not owe money at the passing of the borrower or eligible surviving spouse, even if the outstanding loan balance is more than the value of the house. HUD insurance covers any difference for the lender.

Consideration of historical results. Assumptions about HECM interest rates and projected housing values are often conservative and misunderstood, particularly if not considered as part of a full range of products.

We did our own study of the past 30 years of house prices and interest rates, available in my article Treat Home Equity Like Other Investments in Your Retirement Plan: Look at Its Track Record. You will see that the results were more positive than generally available projections.

One helpful development is that the National Association of Insurance and Financial Advisors (NAIFA) is building a curriculum that will look at this “most underutilized asset” to better understand how housing wealth fits into retirement planning conversations.

(Breaking news: We just received an invitation to a course on “Learn How to Incorporate Housing Wealth into Retirement Planning” from another organization. Do I spot a trend here?)

Retirement planning that builds in housing wealth

Critical to that process is to design a plan with the Three L’s guiding your options and using investment portfolios and lifetime annuities to manage taxes and risks. We’ll cover those topics in the next two articles.

To start the process of making an informed decision about housing wealth, review one plan “with” and a second “without” that resource. Easier said than done since most planning systems are not enabled to do so.

One can also think of the “with” housing scenario as one suited for retirees who want to age in place (favored by at least 80% of retirees) and the “without” as selling your house to generate income or liquid savings and investment dollars.

The first step in the “with” plan is to access housing wealth through HomeEquity2Income, as described in my earlier mentioned article about unlocking housing wealth, by combining HECM with a qualifying longevity annuity contract (QLAC) to provide not only lifetime income, but also a source of liquidity to pay for unplanned expenses.

For the “without” scenario, we assume the house is held until sold at age 85 with the net proceeds invested as liquid savings along with other savings. A multitude of other scenarios are possible, which should be tested with the retirement planning tool.

Comparing ‘with’ and ‘without’ H2I plans

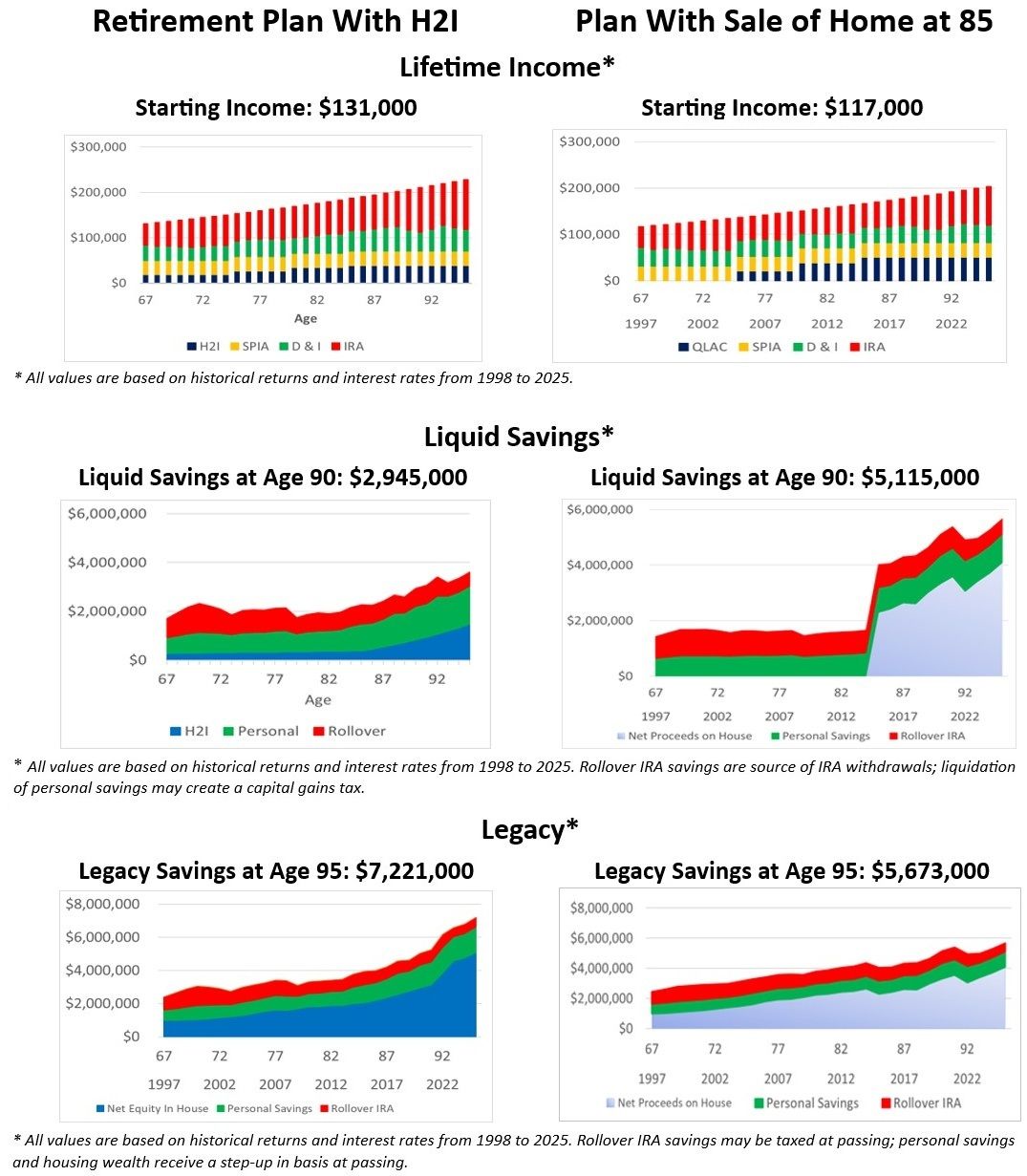

Below is a comparison of two retirement plans for our average retiree, a 67-year-old man with $1 million in each of the three savings sources. The analysis focuses on income, liquid savings and legacy savings.

(Image credit: Courtesy of Jerry Golden)

What we learn from the comparison

The plan “with” H2I is able to support higher starting income ($117,000 vs $131,000) and a higher legacy at age 95 ($7.2 million vs $5.7 million) than the plan “without” H2I.

The primary sources of the “with” H2I advantage:

- HECM drawdowns from age 67 to age 84

- Avoidance of closing costs and taxes on the sale of the home

To be fair, this is a little-explored area and probably needs even more analysis.

Both plans do benefit from the inclusion of lifetime annuities and the reduction of longevity risk, as covered in the unlocking housing wealth article.

The “economic returns on investment” are consistent between the two plans, meaning that the method of aggregating and disaggregating housing wealth is more or less economically neutral.

To me, the advantages of at least considering your home’s equity in retirement planning are clear. An asset that amounts to 50% of the savings built over a lifetime can benefit retirees and their families in the near future and in the long term.

Be on the lookout for the next two articles, which will cover tax efficiency and risk management of planning models.

Building a comprehensive retirement plan requires an understanding of what different products and approaches provide — as well as an understanding of how separate advisers on investments, lifetime annuities and HECM might guide you. We believe it’s well worth it. To find out for yourselves, order a complimentary plan and let us introduce you to a qualified adviser.